Product Teardown: Why Bitcoin Has Failed Its Original Vision

A sharp teardown of why Bitcoin has strayed from Satoshi’s original vision, examining its shift toward digital gold, centralisation, and speculation and what the next generation of crypto must learn.

I have been through and got burned during the crypto winter of 2022. As we watched Bitcoin free-fall by twenty per cent over the last two weeks, the scenes of that winter flashed through my mind.

From an economic or financial yardstick, few would call Bitcoin a failure. No spreadsheet or quant ever predicted a digital token would pull off a trillion-dollar magic trick. Yet when I return to the original premise, the part of the story that mattered before the speculation, it’s hard not to imagine Satoshi shaking his head. Unless, of course, he became a convert after becoming a billionaire.

The revolution was supposed to be decentralised. Instead, it got an IPO.

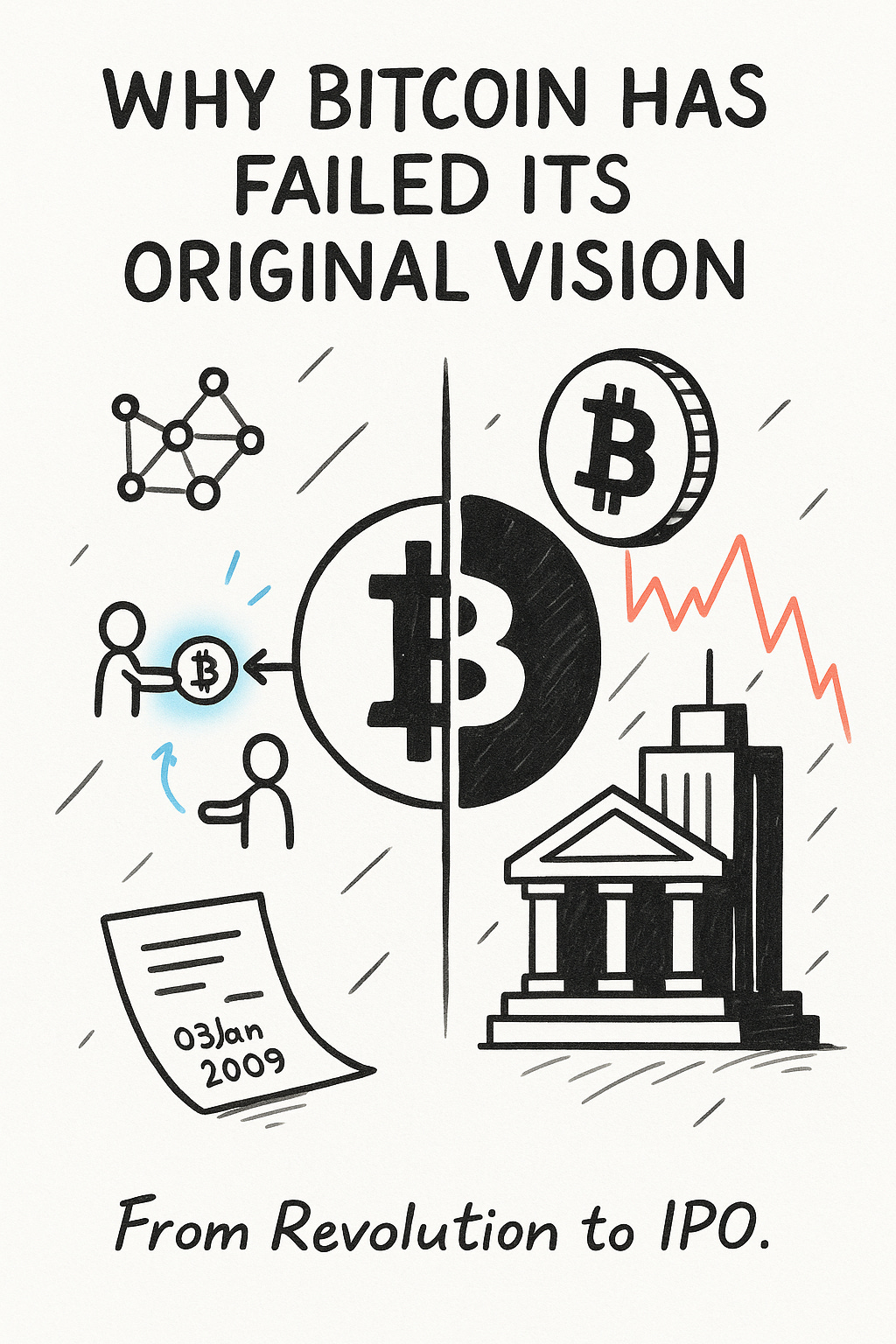

When Satoshi Nakamoto published the Bitcoin whitepaper on October 31, 2008, the message was audacious yet disarmingly simple: build a peer-to-peer electronic cash system that enabled direct online transactions without trusted intermediaries. Sixteen years later, as Bitcoin tumbles from its October 2025 peak of $126,000 to below $90,000, erasing all of the year’s gains, we’re forced to confront an uncomfortable truth. Bitcoin has failed its original premise. Not catastrophically. Not completely. But fundamentally.

1. The Genesis and the Promise

The Original Thesis

Bitcoin didn’t begin as a gold vault. It began as a protest.

The whitepaper wasn’t a hymn about digital gold. It was a blueprint for a payment protocol that could bypass the very institutions Satoshi believed had failed humanity. Embedding “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks” into the genesis block was not poetry. It was a warning shot.

The promise rested on three pillars.

Decentralisation as ideology

Power was meant to be distributed across thousands of nodes, each verifying transactions independently. No kings. No emperors. No HQ.

Peer-to-peer transactions

Money would move directly between people without banks, governments, or payment processors taking their cut.

Financial sovereignty

Users would own their wealth through cryptographic keys, not through an institution’s goodwill.

It was elegant, principled, and radical.

The Meteoric Rise

Then came the early years when Bitcoin behaved exactly like a revolution should.

From zero in 2009 to forty cents in 2010, then thirty-two dollars in 2011, and past one thousand dollars in 2013, Bitcoin gathered believers who saw not price charts, but possibility. The tech worked. The network grew. The narrative wrote itself.

For a moment, it felt inevitable.

The Recent Fall from Grace

Fast forward to November 2025. Bitcoin’s tumble below $100,000, crashing toward $85,000, erased all yearly gains and sent fear rippling across the market. The “digital hedge” now moves in sync with the very risk assets it was supposed to counter.

The anti-system asset now behaves like the system’s mirror.

2. The Great Divergence

From Cash to “Digital Gold”

Somewhere between 2015 and 2017, Bitcoin underwent an identity crisis. The Blocksize Wars cracked open a philosophical divide.

Big Blockers wanted larger blocks, lower fees, and a payments-first Bitcoin.

Small Blockers wanted to preserve decentralisation and security at all costs.

Small Blockers won. SegWit was implemented. The 1MB block limit stayed. Bitcoin Cash forked off. And the victory carved a new identity: Bitcoin as a store of value, not a global payments network.

Academic research confirmed what the community already suspected. A third of Bitcoin holders never transact. Morgan Stanley declared Bitcoin far from Satoshi’s intended payment solution.

The revolution began to ossify.

The Centralisation Paradox

Bitcoin’s greatest irony: an ecosystem built to eliminate centralisation now operates like an oligopoly with better branding.

Six mining pools control up to 99 per cent of blocks. Two of them dominate over half the hashrate.

More than 1,400 “whales” hold over 1,000 BTC each, exerting massive market influence.

Institutions, supercharged by 2024’s ETF approvals, now own more than 28 per cent of outstanding supply.

This isn’t the peer-to-peer financial uprising Satoshi pictured. It’s the New York Stock Exchange wearing a hoodie.

The Environmental Reckoning

Bitcoin’s proof-of-work mechanism has become a planetary problem.

Mining consumed more power than Pakistan’s 230 million people.

Forty-five per cent of that energy came from coal.

CO₂ emissions crossed eighty-five million tons.

Water-intensive cooling drained drought-stricken regions.

Semiconductor demand created PFAS waste with toxic, long-lasting effects.

This is extraction disguised as liberation.

Transaction Dysfunction

Bitcoin’s core utility of providing cheap, fast payments never scaled.

Fees often sit above a dollar and spike under network stress.

Throughput caps at seven transactions per second while Visa handles sixty-five thousand.

Volatility kills usability; a currency that can drop thirty per cent in weeks cannot function as everyday money.

The Lightning Network promised salvation, but by 2025, it had shrunk by twenty per cent from its peak. Complexity, routing issues, and centralisation concerns limit mainstream adoption.

The “peer-to-peer electronic cash” vision is further away in 2025 than it was in 2009.

3. The Landscape Transformed

The Crypto Cambrian Explosion

Bitcoin no longer lives alone on the frontier. Entire ecosystems evolved around and beyond their limitations.

Ethereum built programmable finance, shifted to proof-of-stake, and became the backbone of decentralised applications.

Solana embraced speed and low fees, capturing most new token launches.

Stablecoins and DeFi created tools that look more like the financial system Satoshi wanted to disrupt.

The market moved on. Bitcoin stood still.

Governance Gridlock

Bitcoin’s governance model, or absence of one, has frozen its evolution. The BIP process is theoretically open, but practically dominated by a handful of core developers and major miners. The Blocksize Wars exposed the system’s fragility.

Wikipedia has evolved strong conflict resolution models. Ethereum developed community governance, foundation leadership, and structured proposals.

Bitcoin still resolves conflict through social pressure and ideological trench warfare.

4. Redesigning Bitcoin for Its Original Vision

If we rebuilt Bitcoin today with sixteen years of hindsight, it would look very different.

Dynamic Block Sizing with Safeguards

A protocol that automatically adjusts block size based on demand while monitoring decentralisation metrics would balance scalability and resilience. Blocks expand during congestion but freeze if centralisation rises. Combine this with improved Layer-2 architecture, and Bitcoin becomes usable again.

Formal Governance with Checks and Balances

A three-chamber governance model could distribute influence:

Technical Council (developers)

Economic Council (miners, merchants, holders)

User Assembly (everyday users, one person, one vote)

Major changes would require supermajorities across all chambers. This prevents both developer capture and plutocratic dominance.

Transaction Fee Markets Built for People

A fee structure that prioritises practicality:

Minimal fees for micropayments

Higher fees for large, non-urgent transfers

Fee-burning mechanisms that support long-term sustainability

Balanced incentives to keep validators motivated

Bitcoin becomes usable, not aspirational.

Final Thoughts: The Uncomfortable Truth

Bitcoin succeeded wildly, just not as peer-to-peer electronic cash. It birthed a trillion-dollar asset class, ignited an entire industry, and proved that decentralised consensus wasn’t a fantasy. Yet in the process, it drifted so far from its original mission that it’s hard to imagine Satoshi recognising the creation he set loose.

The tragedy isn’t that Bitcoin failed to scale. It’s that the community chose not to scale it. The movement traded utility for speculation, peer-to-peer payments for digital gold, and financial sovereignty for institutional adoption. Somewhere along the way, the revolution got domesticated.

Maybe this was inevitable. Maybe building a global payments network that is decentralised, secure, scalable, and user-friendly is still beyond what current technology can deliver. But we’ll never know, because Bitcoin stopped trying.

The revolution was supposed to be decentralised. Instead, it got listed on NASDAQ.

Which brings us to the real fork in the road. The challenge for the next generation of crypto builders isn’t technical. It’s ideological. Will we create tools that restore financial sovereignty and enable true peer-to-peer commerce? Or will we continue manufacturing volatile assets for institutions to trade like digital baseball cards?

The choice is ours. But first, we need to acknowledge that Bitcoin has already made its choice. And it wasn’t the one outlined in that nine-page whitepaper sixteen years ago.